Digital Capitalism's "Hidden Abodes"

Examining the Material Politics of the Cloud

Last week I started Techno-Statecraft and opened with a brief overview about the “New Infrastructural Order.” In this initial essay, I take a little more of a deeper dive into the issues of cloud capital on which I will speak of more in the future. In short, I argue that cloud capital is not just digital infrastructure—it is a powerful force reshaping land, energy, and governance, concentrating control in the hands of tech giants while externalizing its social and environmental costs.

The Obscure Geography of Digital Power

The digital economy is built on a vast and growing network of infrastructure—data centers, semiconductor fabs, energy grids, and industrial corridors. Governments and corporations are racing to secure land, energy, and resources to sustain and expand this infrastructure, offering tax incentives, reclassifying land, and cutting regulatory barriers to attract high-tech investment. These decisions aren’t just about technology; they are about power—who controls it, who benefits, and who bears the costs.

Yet, mainstream discussions about the digital economy often remain abstract, focusing on AI breakthroughs, competition between tech giants, or national security concerns. What gets overlooked is the social, material, and spatial foundation of this system—what I refer to as cloud capital. Every financial transaction, AI model, or streaming service is supported not just by a smartphone or computer—the interface that connects to a vast and largely hidden physical network that reshapes economies, environments, and governance in ways that few people can describe, even if its feeling is ever present.

Understanding this social and material geography isn’t just an academic exercise. It is essential to making sense of how cloud capital concentrates power, extracts resources, and reconfigures landscapes. As digital infrastructure becomes a defining feature of contemporary economic and political strategy, we must ask: Who controls the land, water, and energy that make it possible? And what happens to the places and people left navigating the consequences?

What is Cloud Capital?

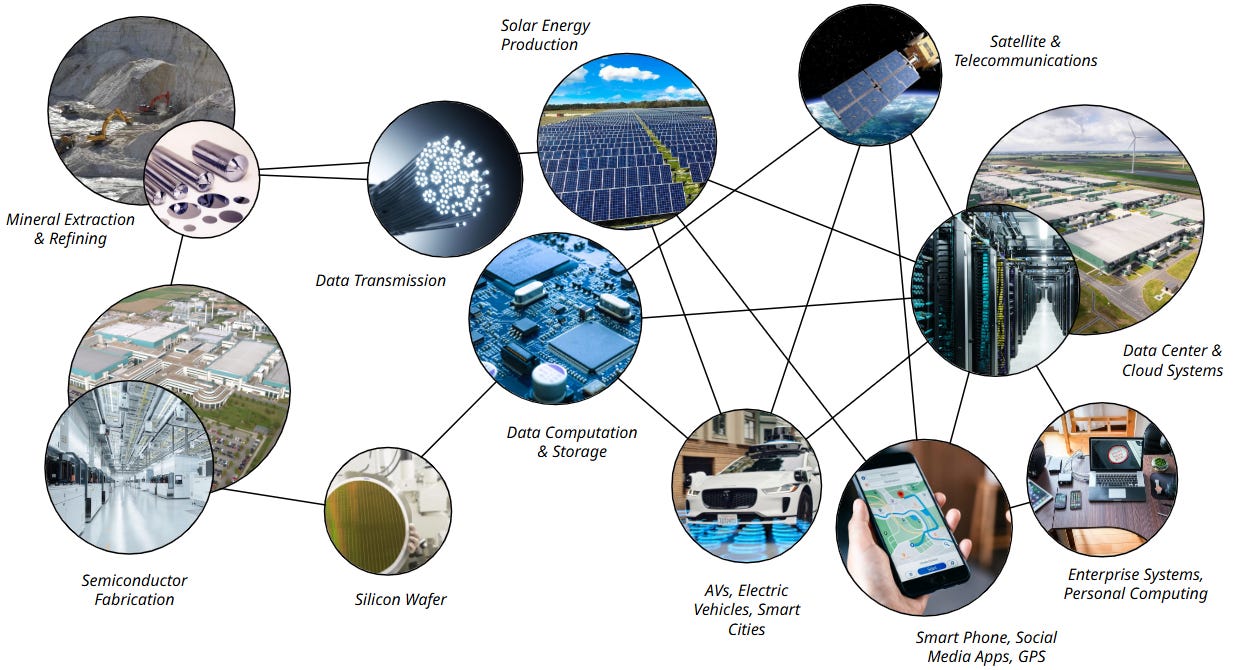

Despite its name, the cloud is anything but airy or weightless. The term originated from the cloud-shaped icon used in network diagrams to represent the internet and complex digital infrastructures abstracted from physical hardware. This physical hardware is owned and operated by a handful of very large firms like AT&T, Sprint, Lumen, with the core services provided by firms like Microsoft, Google, Amazon, and others—turning digital connectivity into a toll road for the modern economy. This consolidation not only centralizes control over critical infrastructure but also enables these firms to extract rents from the vast flows of data, computation, and connectivity that drive modern economies. More than just an asset class, cloud capital fundamentally reshapes how value is generated, extracted, and controlled. It blurs the boundaries between industrial and financial capital, embedding itself in both while redefining their dynamics. At its core, cloud capital is the physical backbone of the digital economy—data centers, fiber-optic networks, semiconductor fabs, advanced chips—to the smartphone or laptop in your hands.

Figure 1: Examples of the networked infrastructures that make up and sustain cloud capital

The essential dynamics are also captured in the term “platform capitalism” on which an enormous amount of scholarship has been built.1 Under this rubric, the rapid expansion of platform firms is driven by the twin forces of financialization and deregulation, which provide speculative capital for aggressive scaling while weakening regulatory constraints. This influx of external funding allows platforms to prioritize market dominance over immediate profitability, leveraging regulatory loopholes to circumvent labor, zoning, and antitrust laws in pursuit of unchecked growth. Cloud computing has fundamentally transformed corporate IT by shifting computing assets from in-house infrastructure to outsourced, scalable services controlled by tech giants like Amazon, Google, and Microsoft.

This shift has blurred the boundaries between back-office and front-office functions, enabled the rise of platform companies, and introduced modular architectures that allow for unprecedented scalability and flexibility in digital operations. Yanis Varoufakis describes cloud capital as a new mode of wealth accumulation—what he calls “techno-feudalism” (think “cloudalism”).2 Its model is one that thrives not on producing goods per se but on enclosing digital space—even outside conventional market mechanisms. Unlike traditional industry, tech monopolies don’t just sell products—they own and control the infrastructure that makes all digital transactions, communication, and computation possible. This grants them the ability to extract rents not just from consumers but from entire economic ecosystems dependent on their platforms, processing power, and networked logistics.

Thus, cloud capital represents more than just a lucrative business model—it is a new form of economic organization that reconfigures both the material and spatial foundations of global capitalism. Yet, this is being driven not only by large corporations, but through state power. While governments lubricate the gears with subsidies, tax breaks, industrial policies, and treat cloud infrastructure as a strategic asset, tech giants leverage financial markets to fuel expansion, securing speculative investments in AI factories, reconfiguring semiconductor supply chains, and capturing more economic activity within their platforms. In the past decade, the big five cloud companies received over 11 billion in subsidies across federal, state and local levels (Figure 2). The CHIPS Act gave out $39 billion in direct subsidies in addition to tax credits for major semiconductor supply chain investments in the U.S.

On top of this, many states have additional CHIPS Act-related subsidies to firms like TSMC which makes nearly all of the most advanced AI server chips, including a $65 billion semiconductor complex in Arizona. The “Big Five,” Amazon, Microsoft, Google, Meta, and Apple, have collectively spent nearly $1 trillion (inflation-adjusted) in capital spending over the past decade (Figure 3), and $151 billion in 2023 alone. As a result of all this, manufacturing and global supply chains are increasingly subordinated to the demands and geopolitical machinations of cloud capital, which acts as a coordinating mechanism, a site of value extraction, and thus a critical realm of conflict.

Yet for all its abstraction, its material demands make it far more industrial than “post-industrial.” Its appetite for energy, water, and land is creating new conflicts over territorial governance, as states, corporations, and local communities wrestle with the consequences of prioritizing digital infrastructure over broader economic and environmental concerns. By embedding itself within industrial and financial capital, cloud capital is not just restructuring economies—it is redrawing landscapes, consolidating power, and rewriting the geopolitics of the digital era. Understanding its material and spatial dimensions is crucial to grasping its full impact.

The Material and Spatial Logic of Cloud Capital

Cloud capital relies on vast physical inputs—energy, water, and land—yet these “hidden abodes” of digital capitalism, where these resources are extracted, distributed, and contested, remain largely obscured to the average person. At the same time, the territorial transformation driven by cloud capital is reshaping cities, rural landscapes, and entire economic systems, often in ways that escape mainstream discourse. Energy, for example, has become a major point of contention, but discussions largely miss the spatial dimension—how energy infrastructures are reorganized, who gets access to power grids, and how these shifts reinforce existing inequalities.

Energy: The Unsustainable Demand of Cloud Infrastructure

Cloud infrastructure is one of the fastest-growing energy consumers worldwide, with hyperscale data centers operating as industrial-scale electricity sinks, often drawing as much power as small cities. In Ireland, for example, data centers used 21 percent of the nation’s energy in 2023, and this share is projected to rise to nearly 30 percent by 2030. This dramatic increase has sparked concerns over grid stability, energy justice, and the environmental impact of large-scale electricity consumption, particularly as artificial intelligence (AI) drives new waves of computing demand.

There is a broader industry push for deeper integration between energy policy and AI development. AI companies, including OpenAI, have identified energy as a major bottleneck for computational expansion, particularly as large-scale machine learning models require exponentially greater amounts of power. Some see nuclear as a long-term solution. Think tanks like the Special Competitive Studies Project, led by former Google CEO Eric Schmidt, have hosted high-profile summits on AI and energy, convening government officials, energy executives, and AI researchers to strategize on meeting AI’s growing power needs.

Despite pledges of sustainability, cloud giants such as Amazon, Google, and Microsoft rely on vast energy supplies, much of which still originates from fossil fuels. These firms sign multi-gigawatt Power Purchase Agreements (PPAs) to lock in direct access to renewable energy markets, yet many of these deals are structured as “virtual” PPAs. This means that while the companies receive renewable energy credits, the actual power used in their data centers may still come from conventional sources. A major infrastructure asset management company, Cohen and Steers, which owns many energy projects for data centers, predicted that natural gas and other “traditional” energy sources would continue to grow along with “alternatives” like solar and wind. Similarly, Goldman Sachs analysts highlight the underwriting of renewables PPAs by cloud companies, but predict even more demand for growth in natural gas infrastructure among other “downstream investment opportunities:”

“We believe supporting data center driven load growth will require investment by Utilities of $50 bn in new power generation capacity. We assume a 60/40 split between gas and renewables, which we expect to drive ~3.3 bcf/d incremental natural gas demand by 2030. While investor interest in the AI revolution theme is not new, we believe downstream investment opportunities in utilities, renewable generation and industrials whose investment and products will be needed to support this growth are underappreciated.”

Furthermore, by marketing their infrastructure as “green,” cloud firms sidestep deeper concerns about grid stability, long-term decarbonization, and the socioeconomic burden of energy transitions—costs that often fall on ratepayers and taxpayers.

Water: The Overlooked Resource of Digital Infrastructure

Water is essential for both semiconductor manufacturing and data center cooling, yet its role in digital infrastructure is rarely discussed. As cloud capital expands, water demand is rising, intensifying conflicts over scarce resources. One of the biggest issues is transparency in water use reporting. While Europe is taking steps to create reporting requirements, the expansion of data centers in Querétaro, Mexico, for example, is fueling concerns over their high electricity and water demands in a drought-prone region, leading to community protests over broken promises on water access.

While tech companies claim to minimize water use, calls are growing for greater transparency and sustainability measures. In fact, both energy and water use information is often carefully protected. When Google established a data center in The Dalles, Oregon in 2006 along the Columbia River, concerns grew over its escalating water consumption, particularly as the region faces drought risks that threaten farmers, environmentalists, and Yakama Nation tribal fishers. A 13-month legal battle ensued after Google and the city, citing trade secrets, resisted disclosing water usage data, but ultimately, records revealed that Google's consumption tripled between 2017 and 2021, reaching 355 million gallons and accounting for 29% of the city's total usage.

Taiwan’s semiconductor industry, a critical link in the global supply chain—including AI chips—faces increasing risks from climate change and water scarcity, as evidenced by the severe 2020-2021 drought that led to stringent water restrictions. Despite prioritization of chipmakers’ water use over municipal and agricultural needs, the industry's heavy dependence on water in drought-prone regions raises concerns about long-term supply chain resilience, but underscores the water-dependent nature of advanced semiconductors that go into the data center building frenzy. As data centers and semiconductor fabs expand, they will continue to drive water demand, forcing governments and industries into new negotiations over who gets access to dwindling supplies.

Land: The Digital Economy’s Physical Footprint

The rapid expansion of cloud capital today demands vast tracts of land, often in rural or exurban areas where infrastructure is available and land costs remain relatively low. Governments actively compete to attract data centers and semiconductor fabs—sometimes vying for the same limited resources—by offering tax incentives, rezoning approvals, and regulatory exemptions, fostering geographic clusters of digital industry. However, the most significant impact is not the immediate land acquisition but the broader, indirect land use changes driven by infrastructure and resource demands. In many ways, land serves as an all-encompassing category that integrates energy, water, and economic development pressures.

For instance, TSMC’s $65 billion semiconductor fab complex in Arizona is said to have triggered a major real estate boom, where speculative real estate cycles have long shaped the region’s economy, further driving conversion of agricultural land to obtain water rights for urban users, but also energy production. The interplay between digital infrastructure, land development, and economic policy warrants deeper examination. Future essays will explore these dynamics in greater detail, focusing on the intersections of land use, energy, water, and the political economy of growth and national security. Key case studies will include:

Virginia’s “Data Center Alley”, the world’s largest data hub, where tax incentives have fueled rapid expansion. Today, more than 70% of global internet traffic passes through its fiber networks.

Oregon’s “Silicon Forest”, where low energy costs and industry-friendly tax policies have attracted data centers, but at the cost of land-use conflicts as rural farmland is rezoned for high-tech development opportunities.

Arizona’s “Silicon Desert”, an emerging semiconductor manufacturing hotspot bolstered by government subsidies and favorable water deals, despite the state’s long-term water scarcity issues.

Taiwan’s “Silicon Island”, where semiconductor production is central to national economic strategy and global supply chains.

For now, it is crucial to recognize that data centers, production facilities, and transmission lines are not just neutral infrastructures but are embedded within specific legal, regulatory, and territorial frameworks. Governed by land laws and taxed based on their physical jurisdiction, these facilities shape and are shaped by uneven geographies of power and capital. This raises pressing questions not only about the abstract distribution of economic and social benefits but also about where the burdens and gains of these infrastructures are materially and politically concentrated.

The Conflicts and Limits of Cloud Capital’s Expansion

Energy and climate concerns have become central to discussions about digital infrastructure, but they are often framed narrowly—reduced to carbon footprints, energy efficiency, or corporate sustainability pledges. The unprecedented energy demands of AI scaling have only recently entered mainstream debate. Yet, this focus on energy metrics obscures a deeper transformation: the way cloud capital is reshaping territory, reconfiguring energy markets, and intensifying land and water conflicts. While nearly every person interacts with these systems—actively through smartphones and laptops or passively through surveillance and data collection—the vast infrastructural expansion enabling this connectivity remains largely invisible.

This infrastructural invisibility is not accidental. Corporate narratives emphasize innovation, economic growth, and national competitiveness, leaving out questions of territorial control, environmental impact, and regulatory capture. The spatial logic of cloud capital—its ability to appropriate land, consolidate power, and reshape governance—is often overlooked because confronting it would force a reckoning with the uneven consequences of its expansion. Furthermore, governments are not merely reacting to these shifts; they are deeply entangled in cloud capital’s growth. The U.S. and many other semiconductor producing countries have passed CHIPS Acts that aim to on-shore or protect advanced semiconductor production within their borders.

Furthermore, the resurgence of this sort of industrial policy is not driven by equitable development—nor solely by corporate influence—but by geopolitical competition. For instance, the UK government has classified data centers as”critical national infrastructure,” enhancing their protection and underscoring the prioritization of digital infrastructure. Meanwhile, financial markets—pension funds, index funds, and utilities—are increasingly tied to the speculative promise of digital infrastructure, including AI. Blackstone, for example, has invested $80 billion in data centers critical for AI expansion alongside energy infrastructure expansion, highlighting the growing entanglement of financial markets with digital infrastructure. Whether these investments will yield sustained returns remains uncertain, but the political and economic commitment to cloud capital is already reshaping energy landscapes and regulatory priorities.

At the same time, more and more friction is arising. Communities and policymakers are pushing back against the rapid expansion of data centers and semiconductor hubs, raising concerns over land use, environmental degradation, and economic priorities. In Virginia, residents oppose new data centers due to excessive noise, grid strain, and land use conflicts. In Ireland, the government temporarily halted new data center approvals over electricity demand concerns. Governments, utilities, and cloud companies are also increasingly at odds, as seen in Virginia’s Data Center Alley, where officials raised property tax assessments to fund infrastructure like roads, power grid upgrades, and emergency services. In response, major tech companies, including Microsoft and Amazon, sued the county government, arguing they were erroneously calculated. Maryland and Virginia also became embroiled in a legal dispute over sharing $5.1 billion cost of upgrading regional transmission infrastructure, with Maryland arguing that Virginia’s data center boom should bear more financial responsibility.

Ultimately, cloud capital is constrained by its dependence on land, water, and energy—resources that are becoming scarcer in key production regions. As competition intensifies, states and nations are scrambling to secure control over the infrastructure supporting AI, finance, and the broader digital economy. This struggle for resources and regulatory advantages is shaping the next phase of cloud capital’s territorial expansion. As communities question the trade-offs, the unchecked growth of cloud capital may become politically unsustainable. If current trends persist, we may see a shift in how and where digital infrastructure develops, with greater scrutiny over its economic and environmental costs. Governments will face mounting pressure to balance incentives for tech firms with public concerns over land, energy distribution, and environmental costs. The key question is no longer which governments can attract cloud capital, but whether they can do so without exacerbating resource conflicts, deepening local opposition, or undermining long-term sustainability.

Reclaiming the Future of Cloud Capital

Recognizing cloud capital as a material and spatial phenomenon forces us to rethink digital infrastructure beyond its surface narratives. If governments are investing billions in digital expansion, whose interests are they serving? If energy grids and water systems are being restructured to support AI and semiconductor production, who is being left out of these decisions?

The future of cloud capital is not predetermined. As public awareness grows, resistance to its unchecked expansion is also emerging—from environmental campaigns against data center sprawl to local fights over water rights and energy access. These struggles will shape the next phase of digital infrastructure, determining whether its expansion deepens inequality or whether alternative models of governance and resource distribution can emerge.

🚀 Techno-Statecraft will continue exploring these issues, unpacking the evolving power struggles over digital infrastructure and the landscapes it transforms.

Key References

Srnicek, Nick. 2016. Platform Capitalism. Polity Press.

Varoufakis, Yanis. 2024. Technofeudalism: What Killed Capitalism. Melville House.