Fabricating Dependency—The Political Economy of the Semiconductor Crisis

How decades of concentrated financial power hollowed out the U.S. industrial base and created geopolitical entanglements

Today, over 90% of the world’s most advanced semiconductors are manufactured in Taiwan, with Taiwan Semiconductor Manufacturing Company (TSMC) alone responsible for nearly two-thirds of global foundry revenue. *It’s also important to note that nearly all advanced AI chips globally are currently produced by TSMC fabs in Taiwan. These chips power not just consumer electronics but also underpin critical infrastructures—from AI and cloud computing to weapons systems and military logistics. The sheer concentration of this production capacity—both geographically and corporately—has triggered alarm among U.S. policymakers, who increasingly cast it as a national security threat and a supply chain “vulnerability,” especially in light of escalating tensions between the U.S. and China and across the Taiwan Strait.

But this dependence is not simply the byproduct of globalization or foreign competition. China didn’t take manufacturing away from the U.S. It is the result of a deliberate, decades-long trajectory of offshoring and disinvestment by U.S. firms, shaped by political choices and the logic of financialized capitalism. The current “crisis” of semiconductor supply is not external to U.S. power—it is a crisis made by it.

Semiconductor dominance in the U.S. was never the outcome of market forces alone. It was built through deep state involvement: Cold War military procurement, federal R&D, and university-based innovation systems. Initiatives like DARPA’s MOSIS program and the public-private SEMATECH consortium were instrumental in constructing a domestic semiconductor ecosystem. Yet by the 1980s and 1990s, U.S. firms—having benefited from these investments—began to dismantle vertically integrated production models, outsourcing fabrication to East Asia to lower costs and satisfy shareholder demands. This shift was not inevitable; it mirrored the broader discipline imposed by financial markets, where long-term industrial capacity was sacrificed for quarterly returns.

Today, attempts to rebuild domestic semiconductor production—most visibly through the CHIPS and Science Act’s $52 billion subsidy package—unfold against a backdrop of systematic disinvestment and financialized retreat. The current push for “reshoring” may be less of a return to industrial strength and more of a state-financed response to a crisis engineered by decades of corporate offshoring and policy complicity. Nowhere is this more evident than in the U.S. dependence on Taiwan and TSMC—not a geopolitical accident, but the culmination of U.S. firms' decisions to externalize fabrication while preserving intellectual property and capital accumulation at home.

TSMC’s rise was enabled by the very firms and policies that dismantled U.S. manufacturing, and it now occupies a position of structural indispensability in the global digital economy. Far from simply a supply chain risk, Taiwan represents the infrastructural expression of a techno-industrial model that displaces the costs of production while consolidating profits through design, platforms, and control. In this article, I trace how U.S. public investment built the original semiconductor ecosystem, how private capital hollowed it out in pursuit of returns, and how today’s techno-nationalist industrial policy risks deepening monopoly and dependency—locking the future of digital infrastructure into a global architecture of asymmetry, extraction, and strategic entanglement.

The Rise and Fall of U.S. Technological Power

The rise of U.S. semiconductor dominance was inseparable from state intervention, including public investment, military coordination, and government regulatory action. Far from being a triumph of market forces or entrepreneurial genius, the industry emerged from a dense infrastructure of public support and oversight. Following World War II, government agencies, military laboratories, and university research centers such as Lincoln Laboratory and Project Whirlwind laid the technological groundwork for semiconductor innovation. The 1956 antitrust consent decree against AT&T, which forced the company to license patents and share research developed at Bell Labs—including foundational work on the transistor—further ensured that critical semiconductor technologies were disseminated beyond a single corporate monopoly. This combination of government funding, procurement, and regulatory policy constituted what Fred Block described as a “hidden developmental state,” making possible the entire industrial ecosystem later claimed as a private sector achievement.1

In effect, the public funding that once nurtured the industry was subordinated to a political economy in which shareholder value overrode considerations of national industrial capacity.

Throughout the Cold War, the federal government actively nurtured the industry. DARPA’s MOSIS project in the 1980s funded a fabrication facility at the University of Southern California, allowing startups and researchers to prototype chip designs without prohibitive costs. But before China was considered a geopolitical and economic security threat, Japan was a major worry for U.S. politicians and firms. SEMATECH, launched in 1987 with Defense Department backing, coordinated research among fourteen U.S. semiconductor companies to counter Japanese competition.2 Federal support helped stabilize collaboration, despite firms’ reluctance to share proprietary knowledge or assign their top talent. By 1997, SEMATECH had become financially independent, but its success was premised on years of public subsidy and state-led coordination.

These investments built an innovation ecosystem that wove together academic research, industrial application, and public funding. As sociologist Manuel Castells noted, the strength of technological clusters depended not just on markets but on the co-location of research institutions, skilled labor pipelines, and government-backed resources.3 Yet as this ecosystem matured and consumer products overtook military procurement for semiconductors and related technologies, U.S. industrial policy increasingly celebrated market primacy while downplaying the state’s foundational role. In practice, public money had laid the groundwork for private accumulation.

By the 1980s and 1990s, corporate strategies began decoupling design from manufacturing. The rise of the “fabless” model—exemplified by new firms like Qualcomm (1985) and later Nvidia (1993)—allowed firms to outsource production to foundries like TSMC while avoiding the soaring capital costs of fabrication plants. This was not just an operational shift but a financial one. Capital markets rewarded asset-light strategies, outsourcing, and short-term returns over the maintenance of domestic production. The foundry model’s expansion paralleled growing shareholder demands for cost-cutting and global supply chain rationalization. This paralleled domestic policy shifts that enabled geographic shifts in manufacturing more broadly.

In this environment, offshoring fabrication to Taiwan and South Korea became a rational strategy aligned with financialized imperatives. Between 2000 and 2020, U.S. semiconductor and microelectronics employment (NAICS 3344) shrank by more than 370,000 jobs, reflecting a systemic disinvestment from domestic manufacturing. This offshoring was not inevitable; it was facilitated by policy frameworks and corporate decisions that privileged financial engineering over industrial resilience—a policy event that I’ll cover in more depth in a separate article. In effect, the public funding that once nurtured the industry was subordinated to a political economy in which shareholder value overrode considerations of national industrial capacity. As U.S. firms offshored fabrication, they locked themselves into reliance on an abundance of external suppliers—setting the stage for today’s structural dependence and geopolitical vulnerability. *Patrick McGee’s Apple in China gives an excellent overview of the role Apple played in building Chinese supply chains.

Change in Semiconductor and Microelectronics Industry Employment (NAICS 3344) in U.S. by CBSA, 2000 to 2020

Distribution of Global Semiconductor Production Capacity in 2023

The Rise of TSMC and U.S. Tech Dependence

The outsourcing of semiconductor manufacturing from the United States to East Asia reached its apex in the rise of Taiwan Semiconductor Manufacturing Company (TSMC). Founded in 1987 as a venture initially aimed at attracting U.S. clients, TSMC pioneered the pure-play foundry model, specializing exclusively in contract manufacturing for firms that designed but did not fabricate their own chips. This model enabled companies like Qualcomm, Nvidia, and Broadcom to shed the capital-intensive burdens of chip fabrication while retaining control over design and intellectual property. This also involved considerable U.S. support as U.S. firms and government were primarily worried about Japanese competition at the time.

Over the next three decades, TSMC consolidated its position at the heart of global semiconductor production. By 2024, it controlled nearly 64% of global foundry revenue, a dominance that extended even further at advanced process nodes like 7-nanometer and 5-nanometer technologies, where TSMC accounted for nearly all available global capacity. This supremacy wasn’t only a function of scale, but a reflection of sustained investments in research, process innovation, and a reputation for neutrality in serving multiple competing customers without direct involvement in chip design—a reputation firms like Samsung and Intel have had difficulty maintaining.

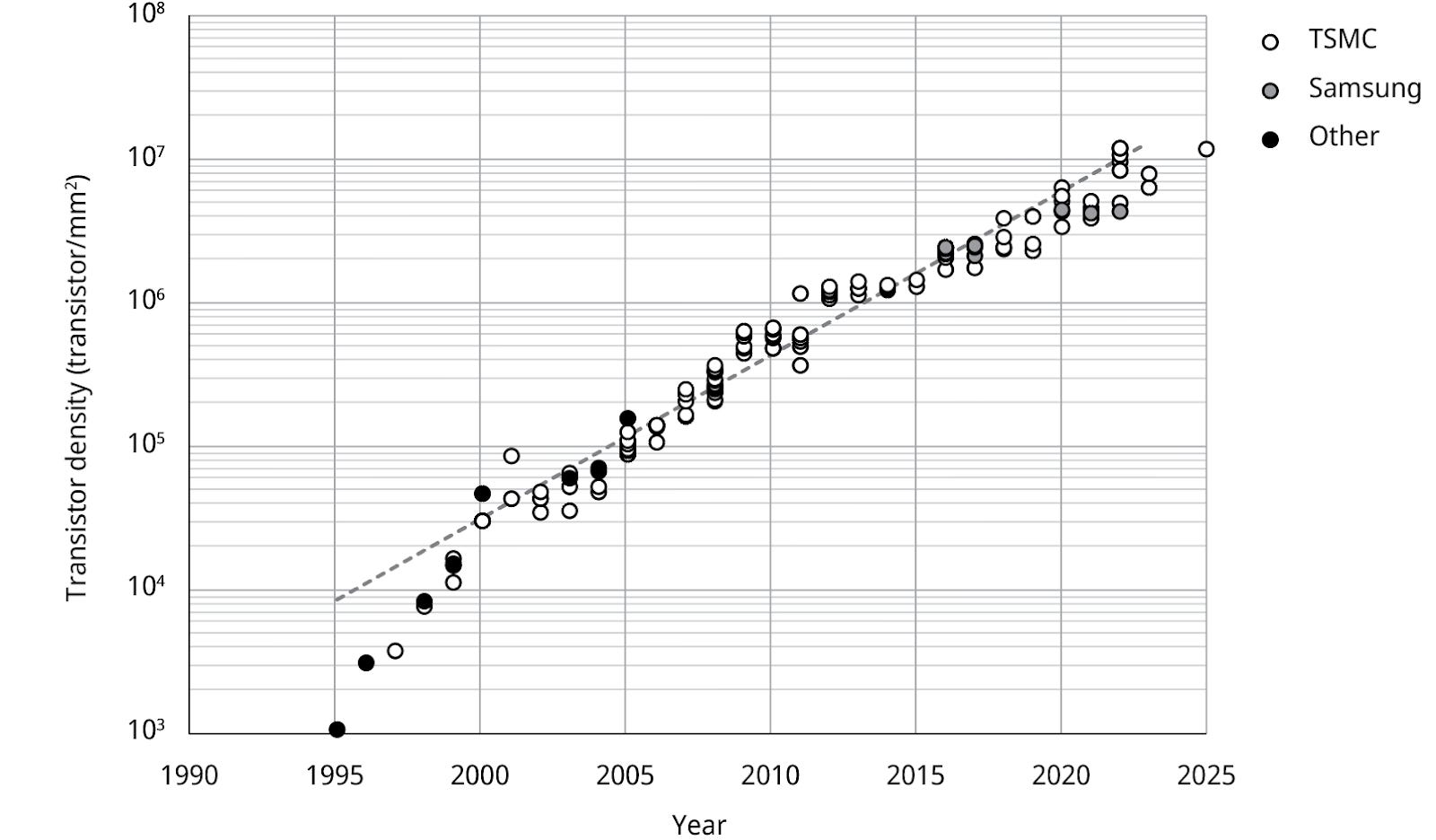

For U.S. tech giants, TSMC became indispensable. The infrastructure of U.S. artificial intelligence, cloud computing, and military systems increasingly rested on chips fabricated in Taiwan. Apple depended on TSMC’s cutting-edge manufacturing for its A-series and M-series chips powering iPhones and Macs. Amazon’s AWS relied on TSMC to produce its custom server chips, including the Trainium and Graviton processors that underpin its cloud and machine learning services. Google used TSMC’s fabrication for its Tensor Processing Units, essential for neural network training and AI services. Microsoft’s Azure Maia 100 AI chip, used to train large language models, was fabricated by TSMC at 5-nanometer nodes. Nvidia’s AI accelerators and AMD’s server processors likewise depended on TSMC’s advanced technologies. Even direct competitors like Intel turned to TSMC to access leading-edge fabrication capacity unavailable domestically. Looking at the chart below, we can see just how dominant TSMC-manufactured GPUs have become in recent years.

Moore’s Law in GPU Production by Manufacturer 1995 to 2025

Rebuilding domestic fabrication is no simple task. TSMC’s dominance also reflected cumulative investments in specialized equipment, materials, technical expertise, and supplier networks developed over decades. Establishing competitive alternatives required not just capital—individual TSMC fabs cost tens of billions of dollars—but an ecosystem of knowledge and infrastructure not easily replicated. At the most advanced nodes, dual sourcing by downstream firms became impractical. Technological complexity, yield optimization (i.e. production of viable chips), and sunk costs meant firms could not easily maintain parallel suppliers. In sum, U.S. firms, and by extension, the U.S. defense and high-tech industrial base, found itself structurally dependent on TSMC—a dependence not incidental but the product of decisions that prioritized short-term returns over long-term industrial resilience.

High-Technology Industrial Policy and Hegemony

By the 2020s, the dependence of U.S. firms grew more apparent to investors, military planners, and government officials alike as investment in data centers and AI infrastructure began to grow. Heightened competition with China and Covid-related supply chain bottlenecks laid bare the price of just-in-time production and hyper-consolidated supply chains. To get a grip on advanced semiconductor production, U.S. congress passed the CHIPS and Science Act in 2022, among other legislation and executive actions by the Biden administration. The Act authorized tens of billions of dollars in federal funding to rebuild domestic semiconductor production, framed as a strategic response to economic insecurity, supply chain risks, and the growing technological rivalry with China. Yet, the CHIPS and Science Act must be understood not simply as an industrial subsidy but as part of a broader trajectory of techno-nationalist industrial policy.

This policy response did not emerge from a single problem, but a confluence of issues. During the Cold War, U.S. technological dominance in semiconductors was built through massive public investment, from Pentagon contracts to DARPA-funded research to university and corporate R&D collaborations. As Henry Kissinger noted, technological power and managerial expertise enabled the U.S. to shape international systems and development trajectories abroad. Yet by the post-Cold War period, U.S. firms had offshored fabrication to East Asia to cut costs and satisfy capital market demands, retaining intellectual property while hollowing out domestic manufacturing. Dependency on external suppliers like TSMC was the result.

China’s semiconductor ambitions, embodied in the Made in China 2025 initiative, reframed this dependency as a national security threat. Although China remained a minor producer of high-end chips, its goal of achieving self-sufficiency by 2030 alarmed U.S. policymakers concerned about losing technological and military advantage. The CHIPS Act emerged as a state-backed attempt to reverse decades of disinvestment by underwriting new domestic manufacturing capacity, research centers, and supply chain coordination.

Yet the Act’s structure reflects continuity with longstanding state-corporate alliances. Of the $52.7 billion authorized, $39 billion was earmarked for manufacturing subsidies, $11 billion for research and development, and $2 billion for defense-specific programs. Oversight was delegated to the CHIPS Program Office within the Department of Commerce and the National Semiconductor Technology Center (NSTC), a public-private consortium coordinating research and workforce development. An Industrial Advisory Committee, comprising leaders from major semiconductor firms, academic institutions, and federal labs, was tasked with guiding implementation. Corporate representation was embedded directly into policy governance.

It would not be inaccurate to say this was an emblematic case of corporate-led policymaking in the name of “public-private partnership.” Parallel advisory bodies, including the President’s Council of Advisors on Science and Technology, institutionalized private sector influence over national technology policy. Figures like Eric Schmidt, former Google CEO, exemplify these entanglements. Through Schmidt Futures, his foundation financed staffing within the Office of Science and Technology Policy and throughout government and policy ecosystems, more illustrative of the pervasiveness of private interests shaping public research agendas than a one-off influence scheme.

The CHIPS Act also aligned semiconductor industrial policy with military procurement objectives. The Department of Defense’s Trusted Foundry and Trusted and Assured Microelectronics programs secured defense-critical chip supply chains. In 2023, $3.5 billion in CHIPS Act appropriations was redirected from research and development toward Intel’s Secure Enclave program, reinforcing the role of domestic incumbents in military supply chains. Additional defense-funded projects, including the Enterprise Parts Management System and the Printed Circuit Board Market Catalyst project, further embedded defense-industrial priorities into semiconductor policy.

These dynamics were not unique to the United States. Similar techno-nationalist industrial strategies were pursued by many others. Europe’s European Chips Act, Japan’s multi-billion-dollar subsidies, South Korea’s incentives to localize materials sourcing, and Taiwan’s ongoing infrastructure investments all aimed to secure positions in global semiconductor value chains. These initiatives reflected a broader geopolitical competition for technological sovereignty, often reinforcing existing hierarchies of dependency and industrial power.

What emerged was a geopolitical industrial boom, marked by state-backed investments of unprecedented scale: Intel’s $100 billion expansion in Ohio, TSMC’s ~$165 billion in Arizona, Samsung’s $98 billion in South Korea, and Micron’s $100 billion in New York. Yet this mobilization of public funds did not disrupt the distribution of power in the industry. Instead, it consolidated the position of incumbent oligopolies while embedding new territorial inequalities—reproducing a global infrastructure of high-tech development structured around monopoly control, geopolitical dependency, and state-capital alliances under the banner of economic security.

Map of Announced Semiconductor Investments, 2021 to 2024

Locked In? Dependency and Consolidation

The semiconductor “crisis” facing the United States is often framed by policymakers as a supply chain failure or a geopolitical risk, a vulnerability exposed by global disruptions or foreign competition. But the real crisis lies deeper: it is the consequence of decades of offshoring, financialization, and political decisions that hollowed out domestic manufacturing in favor of short-term profits and shareholder returns. U.S. dependence on Taiwan’s TSMC was partly geopolitical, partly promoted by large U.S. firms that led the retreat from domestic industrial investment—facilitated by the public policy they promoted that enabled and rewarded disinvestment.

The CHIPS and Science Act is likely poorly constructed corrective to this trajectory, but we can also read it as an extension of it. By funneling over $50 billion in public subsidies to incumbent firms while embedding corporate executives into advisory and governance bodies, the Act reinforces the very structural issues that created the problem. Its alignment with military-industrial priorities and its integration of defense procurement objectives make clear that industrial policy today is not about democratizing production or securing technological sovereignty for the public good. It is about shoring up monopoly control and state-corporate entanglement under the banner of economic security—even more now “national security.”

Globally, the U.S. is not alone. Similar techno-nationalist strategies have emerged across Europe and East Asia, as governments race to secure positions in semiconductor value chains. But these parallel efforts mirror—not challenge—the existing hierarchies of technological accumulation. They entrench a global infrastructure in which a handful of firms and states monopolize advanced manufacturing capacity while peripheral regions remain locked into dependency.

The new semiconductor—and AI—boom promises to transform landscapes, labor markets, and supply chains. But it does so within a political economy structured to prioritize monopoly profits, geopolitical rivalry, and elite governance over public accountability, labor empowerment, or equitable development. Far from heralding a new era of industrial renewal, the CHIPS Act (and whatever comes after) will deepen the very dependencies and inequalities they claim to resolve. If anything has been “secured” in this moment, it is the future of state-backed monopoly power itself—the beating heart of imperial rivalry and competition that led many nations into global war in the early to mid 20th century.

References

Block, “Swimming Against the Current: The Rise of a Hidden Developmental State in the United States”; Block and Keller, State of Innovation: The U.S. Government’s Role in Technology Development. The American developmental state traces its roots to the Smithsonian Institution in 1846, evolving over the 19th and 20th centuries to significantly advance science and technology. Key developments included the Department of Agriculture in 1862, the Agricultural Research Service, and the National Institutes of Health in 1887. Labs under the War Department, later transferred to the Department of Energy, played crucial roles in the Manhattan Project during WWII. Federal labs have driven technological breakthroughs like ENIAC, touchscreen technology, VR, GPS, and genomics, including the Human Genome Project. In 2016, over 300 federal labs accounted for 38% of federal R&D funding. Eleven agencies, including the DOD, DOE, HHS, and NASA, manage significant lab operations with various missions. Key legislation, such as the Stevenson-Wydler Technology Innovation Act, the Bayh-Dole Act, and the Federal Technology Transfer Act, has facilitated technology transfer to the private sector, enhancing the impact of federally funded research.

Wade, “The Paradox of US Industrial Policy: The Developmental State in Disguise.” Wade also critiques the “varieties of capitalism” literature which some claimed the absence of U.S. industrial policy was due to separation of powers. Wade suggests that the decentralized nature of U.S. industrial policy aligns well with the U.S.’s networked production structure and governance system, potentially enhancing industrial policy effectiveness. See Mann, “Has Globalization Ended the Rise and Rise of the Nation-State?”

Castells, The Informational City: Information Technology, Economic Restructuring, and the Urban Regional Process.: 82–88.